Dealing with Debt – A Family’s Story (Part 2)

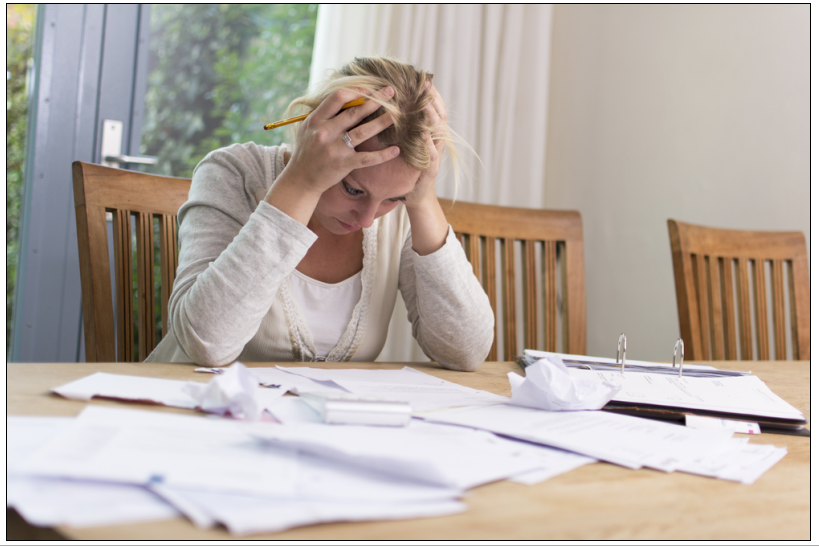

On the way to the wine event, Kathy relayed all of her money issues to her friend Georgia. Kathy was in tears as she arrived at the venue and initially didn't even want to go in.

Kathy was embarrassed by her circumstances, but it still felt good to tell someone. Although Georgia had no idea how it felt to constantly worry about money, she was surprisingly empathic to Kathy's situation.

Once Kathy composed herself and tried to forget about her money issues for a moment, Georgia insisted that she meet with Susan to discuss her situation. Kathy thought that it would be a waste of time. Financial advisors aren’t for people who are in debt or two months away from a foreclosure.

Kathy felt humiliated - she didn't need a stranger judging her. Not to mention, how was she going to afford paying Susan for her time? But when Georgia told her that it didn't cost anything to sit down with Susan, Kathy finally agreed to meet with her.

Kathy and Susan arranged to meet the following Saturday morning.

The First Meeting

Kathy thought it was a little strange that someone like Susan would agree to meet with her on a Saturday morning, but with two jobs and two children, Kathy didn't have any other times available. Susan didn't ask a lot of questions at first – rather, she let Kathy tell her story slowly and calmly. Susan also didn't appear uncomfortable when Kathy broke down in tears a few times during their meeting.

Once Kathy had finished explaining her situation, Susan asked many questions about Kathy’s assets, debts, and income. She also asked where her late husband used to work. Kathy didn’t understand why Susan was asking about this; Kathy needed to address the late mortgage payments and figure out a way out of debt (if that was even possible).

At the very least, Kathy had to figure out how she could at least tread water and not feel like she was drowning all the time.

A Second Opinion

After they were done, Susan had a few suggestions. Although it was a long shot, Susan wanted Kathy to check with John’s former employer. Before her husband became a pilot, he had worked for a shipping company, Priority Courier, for approximately ten years.

John didn’t particularly like working for Priority Courier, but the pay and the benefits were good and he continued working for them until he became a full-time commercial pilot. Susan asked if John had paid into a pension while he worked for Priority Courier.

Kathy didn’t know. She hadn’t received anything in the mail from Priority Courier in years, so she assumed there wasn’t anything relevant coming from them anymore. But, now that she thought of it, Kathy remembered something…perhaps she had forgotten to tell Priority Courier of her change of address when they bought the new house five years ago!

Kathy was so busy during that time, it was very possible she had forgotten to tell Priority Courier about their new address. Susan wanted Kathy to contact Priority Courier’s human resources department right away and ask if John still had any pension with them. Susan counselled that if John did, and if Kathy was the named beneficiary, perhaps there were funds that Kathy could access.

A New Hope

With those funds from the pension, Kathy could make the mortgage payments and other debts.

Susan agreed to meet Kathy again the following Saturday morning, while Kathy promised to give Priority Courier a call first thing Monday morning.

After leaving the appointment, Kathy felt hopeful for the first time in a long while.

On Monday morning, Kathy found a few moments to call Priority Courier. As quickly as it had arrived, her hope quickly dissipated once she spoke to the human resources person at Priority Courier. Although John did have a pension worth $50,000, and Kathy was the named beneficiary, the operator advised that the funds were, “locked in.”

In other words, Kathy wouldn’t be able to access the funds until she was 55.

Despite this the operator agreed to email a statement to her, so she could review for herself.

A Second, EXPERT, Opinion

On Saturday morning, Susan met with Kathy to review the statement sent to her by Priority Courier. Susan advised that she thought the operator Kathy had spoken to was mistaken. Susan informed Kathy that many pensions are “locked in”. In other words, they may not be able to access the funds until later in life. It depends which province the pension is governed by, but typically it could be as late as age 55 for most provinces.

However, some pension plans are just group RRSPs. That means they’re governed by the same set of rules as traditional RRSPs. With RRSPs, you’re allowed to withdraw the funds whenever you want. Ideally, RRSP funds should only be taken out when you’re retired (presumably when you’re in a lower tax bracket).

In Kathy’s case, it would be perfectly reasonable to withdraw from an RRSP pre-retirement, given the circumstances. Susan advised Kathy that she would be taxed on the money she withdrew, but that any withdrawals would have tax withheld. That meant she wouldn’t have a huge tax bill the following spring.

Kathy was elated to know she wasn’t going to lose her house, but she still had other nagging concerns.

How could she manage her other debts? She barely had enough to get by each month – would that ever change? It wasn’t as though Kathy was frivolous with her money – in fact, it was quite the opposite. Meanwhile, many of her friends went on three vacations a year, had a cabin at the lake, and still complained about not having enough money.

It was hard for Kathy to listen to those friends, when she was being overwhelmed by the costs of her and her daughters’ necessities. Kathy was doubtful that Susan could help manage her cash flow, but she was willing to try.

-----

By taking Susan up on an offer for a free consultation, Kathy was able to save her house.

That’s a massive stress relief – and could have been rectified sooner if an expert opinion had been available to her from the beginning. The financial world is, frankly, confusing – it’s certainly not designed for easy navigation by the average adult!

By reviewing old details that had never occurred to Kathy, and offering a solution based on that review, Susan immediately offered major value.

But debt is often a multi-faceted issue – and it would take more than one recommendation to fix Kathy’s debt issues.

That’s why she was working with an expert. What other ideas could Susan offer?

Stay tuned for the last chapter in our series on debt.

As always, thanks for reading.

Brent Misener, Misener Wealth.

Brent Misener is a Financial Advisor with Raymond James Ltd. The views of the author do not necessarily reflect those of Raymond James. Statistics and factual data and other information are from source Raymond James Ltd. (RJL) believes to be reliable but their accuracy cannot be guaranteed. Information is furnished on the basis and understanding that RJL is to be under no liability whatsoever in respect thereof. It is provided as a general source of information and should not be construed as an offer or solicitation for the sale or purchase of any product and should not be considered tax advice. Raymond James advisors are not tax advisors and we recommend that clients seek independent advice from a professional advisor on tax-related matters. Securities-related products and services are offered through Raymond James Ltd., Member - Canadian Investor Protection Fund. Insurance products and services are offered through Raymond James Financial Planning Ltd., which is not a Member - Canadian Investor Protection Fund.